One of the many choices that come when you start a job is whether to participate in your employer-sponsored retirement account. If you decide to take part, the next decision is whether to contribute to a Roth or a traditional account. Here are some things to keep in mind as you make that important selection.

FREE May 20 MOAA Webinar: Is a Roth Conversion Right for You?

Join MOAA and special guest Col. Brian “ALF” O’Neill -- retired Air Force fighter pilot and founder of Winged Wealth Management and Financial Planning LLC -- to learn who should consider a Roth conversion, which accounts to use, and how (and when) to execute the conversion, with a special focus on the new Roth conversion option offered in your Thrift Savings Plan.

Know the Difference

Roth and traditional setups differ in how they treat taxes for your retirement account, whether it’s in the Thrift Savings Plan or your employer’s 401(k)/403(b)/457(b). The main difference is when you pay taxes.

With a traditional account, you make contributions from your paycheck before taxes are taken out. This helps you in a couple ways: First, it gives you a tax break on your current taxes, since it reduces your taxable income. It also allows your money to grow free of tax until you’re ready to take it out after age 59½. But once you start taking distributions from that account in retirement, you will pay income tax on both the contributions and their earnings.

[RELATED: What New Tax Laws Mean for Your Charitable Contributions]

Contributions to a Roth account, however, are made with after-tax dollars. You won’t save anything on your tax bill now, but when you retire and take distributions from your account, the distributions — including earnings — will be tax free.

While not every employer offers a Roth option, they are becoming more popular, with an estimated 93% of plans offering it (even though just over 20% of workers take advantage of it).

Now vs. Later

Conventional wisdom says that the younger you are and the less you earn, the more sense it makes for you to contribute to a Roth retirement account, since you will presumably be in a higher tax bracket in the future and it’s better to “prepay” your taxes now at your current tax rate.

But that doesn’t mean that mid-career and even more “seasoned” folks can’t benefit from contributing to a Roth.

One helpful way to compare these two tax treatments is to use a calculator, such as the one found on MOAA’s website. You can plug in your current age, your projected age at retirement, and your annual contribution to get an idea of how the Roth and traditional options stack up.

I plugged in a starting age of 35 with a retirement age of 65 and chose to max out the annual contribution, which is currently $24,500 for those under age 50 and $32,500 for those 50 and older. Those age 60 to 63 can contribute up to $35,750 under special catch-up contribution limits in place for 2026.

MOAA’s calculator assumes that your current tax rate is higher now than at retirement (24% vs 22%). It also assumes that any tax savings you are realizing from your traditional accounts this year will immediately be reinvested.

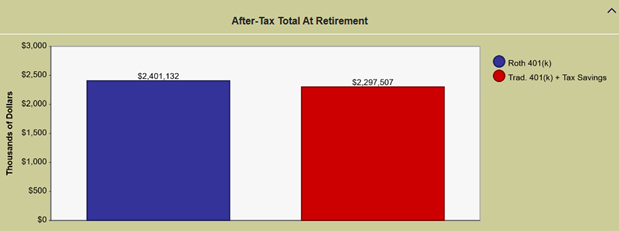

In this scenario, the outcome is roughly the same, with the after-tax total at retirement in the Roth account estimated to be $2,404,132, about $103,000 more than the traditional account. Here’s a look at the chart:

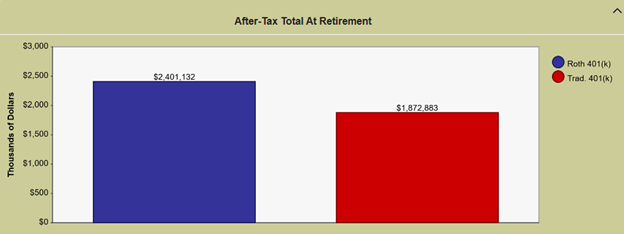

But most folks don’t reinvest those tax savings. If we deselect the option to “invest annual tax-savings generated by traditional account,” we see a vast difference (more than $528,000) between the balances in the two accounts:

And it is not a given that you will be in a lower tax bracket in retirement. Many military retirees with a pension, Social Security, and other investment income coupled with fewer tax deductions find themselves in a higher bracket.

And while the current top marginal income tax bracket stands at 37%, the rates eventually could end up higher: The top rate was 50% in 1980, for instance, and a whopping 91% in 1963.

Want to run your own numbers? Visit the calculator page yourself.

[MORE MATH: MOAA.org/Calculators]

Notes to Remember

Those with earned income may also be able contribute to Roth or Traditional Individual Retirement Arrangements (IRAs). The tax treatment of these individual accounts is similar to the Roth and traditional employer accounts described above, but you are able to contribute a much smaller amount (for 2026, $7,500 per year, and $8,600 if you’re 50 or older).

This article was originally published in August 2022 and has been updated. Last update: April 2026.

Money Matters. Let MOAA Help.

Our finance and benefits experts provide well-researched and relevant information to our members. Check out upcoming financial webinars, or access our webinar archive (Premium and Life members only) for more.