(This article by Kimberly Lankford originally appeared in the February 2021 issue of Military Officer, a magazine available to all MOAA Premium and Life members. Learn more about the magazine here; learn more about joining MOAA here.)

The Thrift Savings Plan has always been a valuable benefit for the military, and recent changes make this low-cost and tax-advantaged account even more attractive. Servicemembers in the Blended Retirement System (BRS) can receive matching contributions from the government. New withdrawal rules give retirees more flexibility to access TSP money. And many people still haven’t taken advantage of the Roth TSP, which grows tax-free for retirement.

“The TSP for the military is the first and best option to save for retirement,” said Lila Quintiliani, an accredited financial counselor and the program manager for Military Saves. “With the automatic savings, the TSP can just come out of your paycheck each month and you won’t even realize it.”

Those automatic contributions can become even more valuable during a time of market volatility, such as the coronavirus pandemic. By contributing a fixed dollar amount from each paycheck, you avoid trying to time the market; plus, you’ll buy more shares when the price is down.

[RELATED: Here’s What You’re Saving at Military Commissaries]

“This is a historic opportunity to build wealth,” said Lt. Col. Shane Ostrom, USAF (Ret), CFP®, program director for finance and benefits at MOAA. “If I had this opportunity in my 20s and 30s, this would have established a baseline of wealth that would have soared over the next decades.”

Meanwhile, older people need to assess their TSP investments to make sure their allocations still match their timeframe and risk tolerance. Whether you’re new to the military, have been serving for years, or have retired and plan to start taking withdrawals soon, it’s important to review your TSP account and make the most of the new rules and strategies.

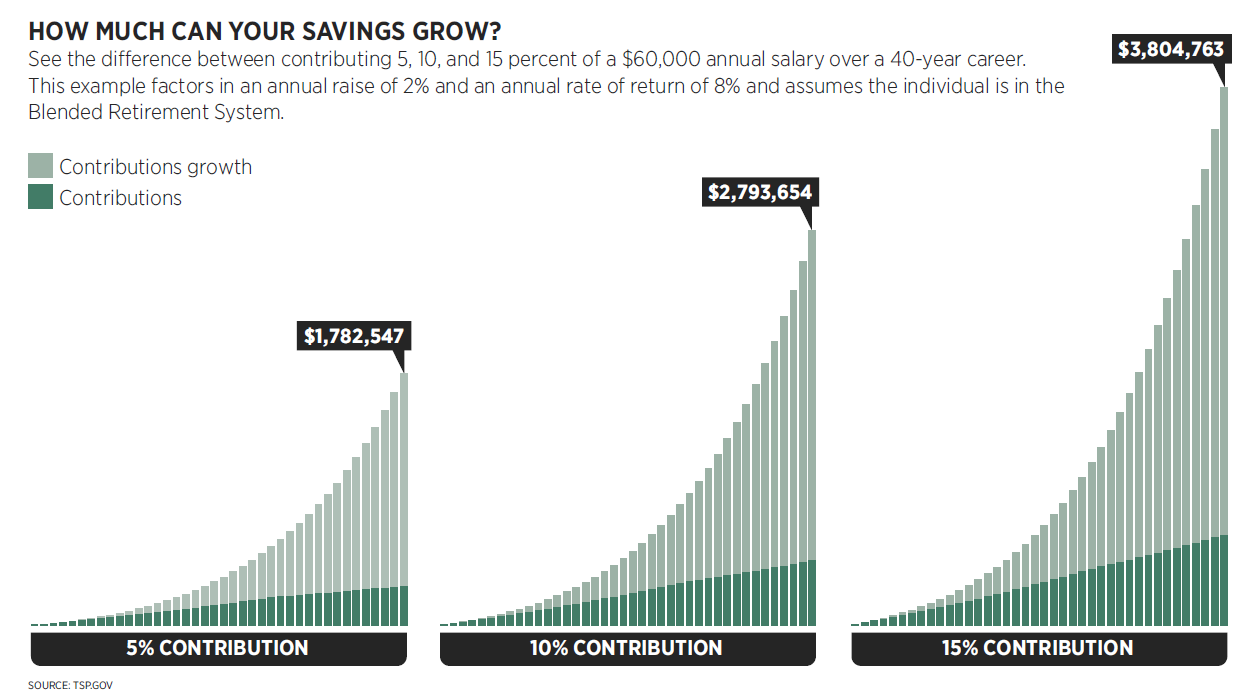

Click here to open the above graphs in a new window.

New Benefits for Contributing to the TSP

You can contribute up to $19,500 to the TSP in 2021 — or $26,000 if you’re 50 or older. If you joined the military between 2006 and 2017 and opted into the BRS, or if you joined in 2018 or later, then your service contributes 1% of your pay to the TSP and matches your contributions for the next 4% of your pay. You need to contribute at least 5% of your pay to get the full match.

“If you’re looking for a place to start, the absolute minimum would be to contribute 5% of your income if you’re in the Blended Retirement System, or else you’re leaving money on the table,” said Col. Curt Sheldon, USAF (Ret), a certified financial planner and enrolled agent in Alexandria, Va., and MOAA Life Member. “Take advantage of that 5% of free money, and then ultimately try to get to saving 10% of your income.”

If you were automatically enrolled in the TSP in 2018 or later, then 3% of your basic pay is contributed to the TSP. You’ll need to increase your contributions to 5% in your MyPay account to get the full match. Auto-enroll contributions increased to 5% for new participants starting on Oct. 1, 2020.

[RELATED: 4 Methods of Managing Risk]

The TSP is valuable even if you’re in the legacy retirement system and don’t receive a match. If you stay in the military for 20 years, your pension is based on 50% of your basic pay, not counting your housing allowance (40% of your basic pay under the BRS). If you don’t stay for 20 years, you won’t get a pension under either retirement system, so you’ll have to rely on your retirement savings. Either way, add to your account whenever you can.

“If you get a promotion, pay yourself first and bump up your contribution rate,” said Cmdr. Didi Dorsett, USN (Ret), a certified financial planner in Occoquan, Va. “If you’re deployed, you can give yourself a quick surge.”

The contribution limits rise when you receive tax-exempt income in a combat zone — $58,000 in 2021 — and that money goes in and comes out tax-free.

Roth or Traditional Contributions?

Traditional TSP contributions are pre-tax, grow tax-deferred, and are taxable when withdrawn. Roth TSP contributions don’t reduce your taxable income, but withdrawals are totally tax-free in retirement.

The Roth is better if you think you’ll be in a higher tax bracket in retirement, which often happens when you aren’t receiving a tax-free housing allowance and other benefits (also, recent tax cuts are scheduled to expire after 2025).

“If you’re a junior officer, especially if you have a family, you are probably in the lowest tax bracket that you’ll see throughout your life,” said Quintiliani.

A Roth TSP also diversifies the tax situation of your retirement income. Pensions and traditional TSPs, 401(k)s, and IRAs are taxable when paid out. The Roth TSP gives you a bucket of tax-free money to tap in retirement.

“One thing I hear from people who are retired is that they wish they would have had an opportunity to put more money in a tax-free account because now everything they’re getting is taxable,” said Ostrom.

Investing Strategies

The TSP is known for its low fees and simple investing options. You can choose from five index funds — investing in large companies (C Fund), small and medium-sized companies (S Fund), international companies (I Fund), bonds (F fund) and government securities (G Fund). The average expense ratio increased recently but is still quite low (0.042%, which is 42 cents per $1,000 invested). You can create a portfolio based on your timeframe and risk tolerance.

“The younger you are, the more C, S, and I you should own. In your 20s, it should virtually all be stock. As you age, you can slowly add in more stable F and G,” said Lt. Col. Patrick Beagle, USMC (Ret), CFP®, owner of WealthCrest Financial Services in Springfield, Va.

Instead of making these choices yourself, you can invest in the L fund, a target-date fund that creates a diversified portfolio of the other funds based on your investing timeframe. You choose the date closest to when you plan to withdraw the money, and the fund gradually shifts to more conservative investments through time.

The L fund can also help you avoid panicking and selling at the wrong time in a volatile market.

“If someone is tempted during volatile times to make adjustments and make emotional decisions, then they really need to take a deep breath and think of their long-term goals,” said Capt. Ted Digges, USN (Ret), executive director of the Penn Mutual Center for Veterans Affairs at the American College of Financial Services (and a MOAA Life Member). “The nice thing about the L fund is it’s good for those that lack the time, the interest, or the expertise to get involved with those kinds of decisions.”

The L fund tends to be more conservative than other target-date funds. Beagle often recommends choosing a later target date to keep more money in stock funds for longer.

New Withdrawal Options

In the past, you could only take one partial withdrawal from the TSP, and then you either had to withdraw the remaining balance in a lump sum, convert it to a life annuity, or sign up for monthly payouts that could only change once per year. But new rules made TSP withdrawals much more flexible, like 401(k)s: You can now take withdrawals whenever you’d like, or you can set up and change installment payouts at any time.

There’s now less of a reason to roll your TSP into an IRA when you leave the military. In fact, Ostrom often recommends rolling over money from other employers’ 401(k)s into the TSP after you leave those jobs.

“The TSP is a bit unique by allowing you to move money into it after you’re no longer employed there,” said Ostrom. “You get the cost savings, you have the simplicity, and you’re familiar with the plan.”

Although you can choose between your Roth and traditional account, you can’t specify which TSP investments to tap for withdrawals — the money is taken pro rata from each of your investments. You can roll over your TSP to an IRA at that point and control which investments to tap, said Dorsett.

Kimberly Lankford is a freelance financial writer and military spouse in Lynchburg, Va.

Support MOAA Charities

Donate to help address emerging needs among currently serving and former uniformed servicemembers, retirees, and their families.