MOAA National

2024 MOAA Charities Golf Classic

Register for our annual event and support members of the uniformed services community in need.

Register for our annual event and support members of the uniformed services community in need.

Begin your research on senior housing of all types across the nation.

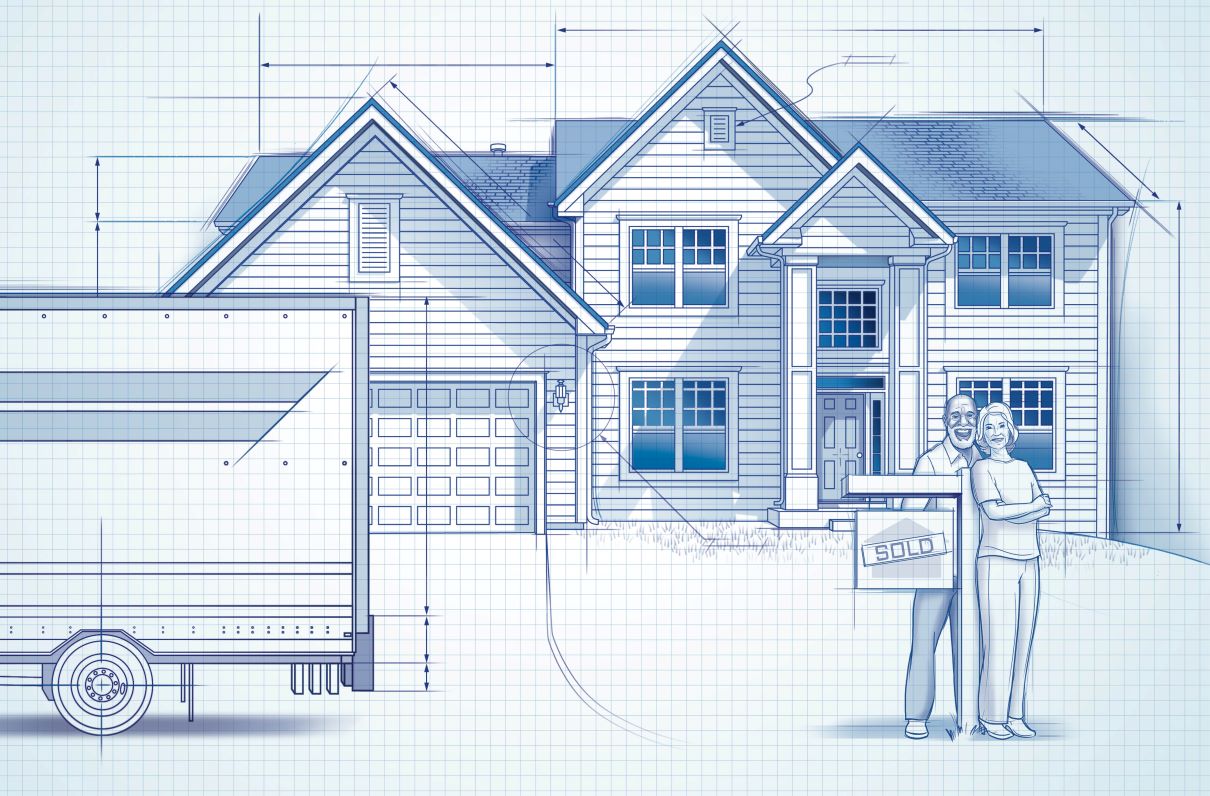

Maximize your profit with advice from experts nationwide.

Learn about recent legislation that may affect your service-earned benefits, along with MOAA's priorities for the upcoming National Defense Authorization Act.

Get what you deserve in your next salary negotiation.

Artificial intelligence can set you apart from the rest of the job-seeking crowd. Find out how.